A biotech slow liquidation

Combined with a higher quality business

I have been on a winning streak with biotech stocks in the past few years. I actually remember thinking 2 years ago that I would not even look at them, but when a sector gets cheap it is just too tempting not to, and I am not regretting it so far.

The stock I have today is a slow selling off of a lower quality low growth business to focus more on the higher quality business. The sale proceeds from selling its low growth medical devices business could easily surpass the company’s current enterprise value based on sales made in the past year. I think this stock is a relatively straight forward double with multiple catalysts to unlock value.

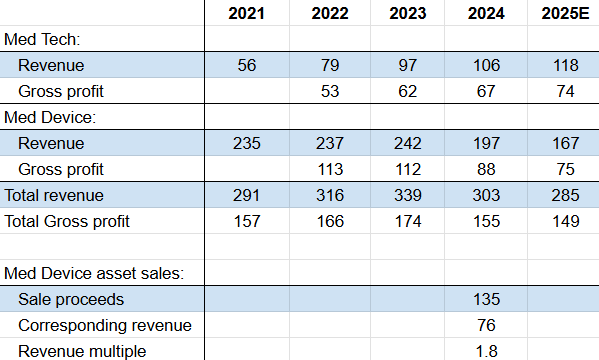

The company’s name is Angiodynamics (ANGO). I had this one on my watch list because of this VIC write-up, but when I saw that Citrini liked it (and the sector as a whole) and they settled their lawsuit, I had a closer look at it. The business can be split up into Med Tech (double digit growth) and Med Devices (low single digit growth). Management has said that they will be “active portfolio managers” and “focus on the Med Tech business”. They have so far made two asset sales in FY 2024 (which ends June 1st). The Med device business will still be the majority of revenue:

Management is not aggressively liquidating the Med Device business, but seem to be opportunistically selling portions of it (hence the “active portfolio manager” phrasing). The company currently has a net cash value of about $50m and an EV of $225m while being roughly cash flow break even. If they sell the remaining Med device business for a similar multiple it would generate proceeds of $288 million.

The Med Tech business

This is the most interesting part as the Med tech business could easily be worth 3-4x revenue, more than the current enterprise value. This segment is made out of:

Auryon, responsible for about $50 million in revenue in 2024. Growing 12% and approved for atherectomy in peripheral arterial disease (PAD). This is a $1 billion global market. The company is trying to get Auryon approved for small vessel Thrombectomy by early 2025. This is a $2.5 billion global market. Auryon is the only atherectomy device that is able to treat hard and soft calcifications above and below the knee as well as in-stent restenosis. So this is a highly differentiated product.

Nanoknife, This is an older device, currently approved for Pancreas cancer and looking to get specific approved for treatment of Prostate cancer (fairly likely to happen at end of 2024). Revenue of ~$26 million with growth of 30% in 2024 with a Prostate TAM of $2.6 billion.

Alphavac and Angiovac, the least exciting portion of the med tech business with about $32 million in revenue if we annualise Q4 results. And growth was flat. These devices are for the treatment of large vessel thrombectomy and the removal for clots in the left atrium. This is a several billion $ market but differentiation is low.

The more mature Med device business is likely generating around 30% operating margins on a standalone basis while the Med Tech business is currently loss making. I am most excited about prospects of Nanoknife for Prostate cancer:

This treatment greatly reduces the odds of getting erectile dysfunction (44-77% odds with radiation and surgery currently) or incontinence. And allow for earlier treatment (since patients often wait due to high odds of these side effects).

I see multiple catalysts for a rerating here:

December 2024 approval of Nanoknife for prostate cancer and Q1 2025 small vessel Thrombectomy approval for Auryon. This would add multiple billion $ in TAM with highly differentiated products. I think Nanoknife approval is very likely as results from the PRESERVE trial were pretty good with fairly low adverse effects, I have a harder time handicapping Auryon approval.

Level 1 CPT codes for Nanoknife Prostate cancer treatment. This would happen after FDA approval and make it easier to get reimbursed (which will increase pricing power and sales growth). Management is unclear on the timeline here, so I expect this to take more than a year.

$10-15 million cost cutting program from outsourcing manufacturing + $30m R&D expenses being greatly reduced after 2025. Recently though the company issued a press release they will keep 40% of the factory work force related to their current products. So this number will likely be lower.

Accelerated higher gross margin revenue growth after 2025 for Med Tech business. This will flow straight to the bottom line.

Likely profitability FY 2026.

Further Med Device asset sales.

Further buybacks (currently $15m program in place).

Possibly a sale of the Med Tech business somewhere down the road.

The CEO also has been buying shares this year, 30k shares in total for $6-7.

The plan is to hold ANGO for 2 years, see if there is indeed an inflection in 2026 and hope for more asset sales and buybacks. I think upside is easily 100-150% with relatively little risk and a lot of potentially positive news to send the shares higher.

I will probably sell if the Med Device segment starts shrinking beyond a few % and beyond some QoQ variance or if Med Tech is flat 3-4 quarters in a row. Further risks are obviously the above list of bullet points not working out.

Disclaimer: Readers of this blog should do their own due diligence before buying or selling any of the mentioned stocks, since I have been wrong before and cannot guarantee all information in this write-up is 100% factual. I may buy or sell the above mentioned stocks at any time. Past success is no guarantee for future success. Some of the stocks mentioned might have poor liquidity, so make sure to check average daily trading volume before buying or selling anything. I am not your financial advisor.