G & M Holdings

Is the market asleep on this one?

G&M (HK:6038) has an enterprise value of about zero, TTM PE of 5.6x, and a dividend yield of almost 11%.

By the looks of it G & M seems to have reached the bottom of the cycle probably 6 months ago.

David Webb holds a significant stake in one of its inferior and more expensively priced competitors.

Average trading volume of only USD$1300 per day

G & M holdings is in the niche market of designing, installing and maintaining podium facades and curtain walls in Hong Kong. This report describes the industry rather well. Podium facades and curtain walls are the outside panels on high rise buildings. Podium facades are at the bottom while curtain walls are higher up. G&M is mostly in the Podium facade business.

Overview of industry size:

With revenue averaging several 100 million in the past years, G & M seems to have between 10-20% market share in podium facades. Recently they were forced to take on more curtain wall projects, and margins seem to have suffered. But historically operating margins were about 20-25% with very healthy double digit ROIC.

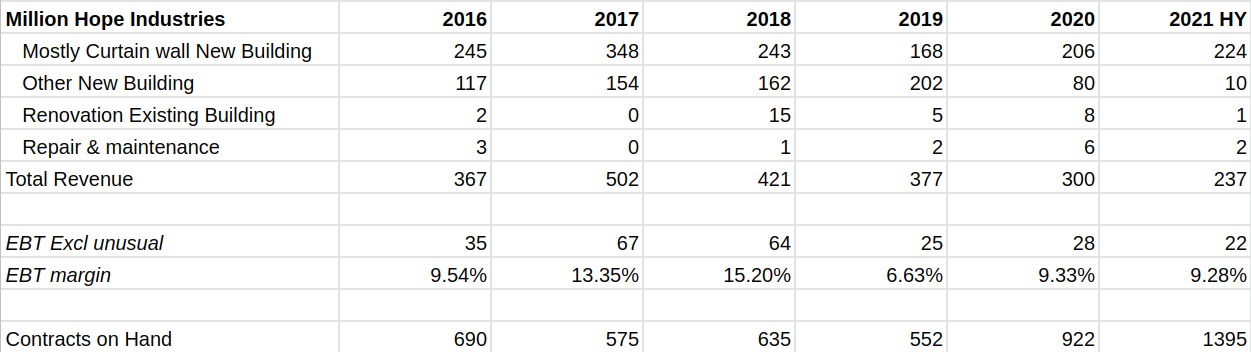

Million Hope industries (HK:1897) is a competitor in curtain walls, with much lower market share. Their EV is also zero but has a TTM PE of 12x and David Webb is a major holder. But this is a much less attractive business, likely because it is not as niche. Operating margins have hovered around 10% and ROIC has slumped to below 10% recently.

What makes both stocks really interesting is that they disclose the contracts they have signed over the coming 2-3 years. Due to new initiatives to boost housing supply by the HK government, those contracts on hand have nearly doubled in 2020 (click to zoom in):

And this is what financials and contracts on hand looked like for Million Hope:

For G & M this means that if these contracts are spread out over 2-3 years (which is usually the case), they win no more new contracts in the coming years (unlikely), and margins on these contracts average 15%, net profit will be over HK$100 million in the coming 3 years.

If we are a bit more optimistic and assume 20% margins, and assume they win another ~HK$200m in contracts in coming 3 years, net profit will be a total of HK$180m the next 3 years, and the stock currently trades at a PE of 2.2. I think 15-20% operating margins is a conservative estimate, since historically Podium Facade margins used to be around 20-25%. Given that dividend payout was >50% in the past 3 years, it seems likely the forward dividend yield on this stock would be somewhere between 15-30%.

So why is it still this cheap? The only major risk I can see is labor costs. Unemployment has always been very low, and labor costs have increased in low double digits. Labor costs were about 17% of revenue in 2019 for G & M and 13% of revenue in 2016. Although the lower margin Curtain wall projects likely caused some of this as well. In Million Hope annual reports, they often complain about this as well. But even if G&M’s current order book has only 10% operating margins, that still means they will earn half, and likely pay out 1/3 of their market cap in the coming 3 years. Not a bad bear case to have, especially considering enterprise value of this stock is zero, with their HK$132m net cash position on hand. You are basically buying a net net that will also be likely a great business in the coming years.

Another potential risk is that G & M is controlled through a holding company called Luxury Booming, which owns 75% of G & M and is held by mr Lee who owns 75% of Luxury Booming and mr Leung who owns the other 25%. Hong Kong law protects minority holders though, as 90% of minority holders need to agree to a takeover. So a take under seems unlikely here. Risks of any fuckery here is also mitigated by the large dividend payouts.

I think really the main reason this is as cheap as it is, is because of the terrible liquidity, zero promotion by management, small market cap and even smaller float, Covid-19 and all the negative news surrounding Hong Kong and China.

Despite the terrible liquidity of this stock, I have managed to build a significant position over the past months, and I am long at an average price of HK$0.136 per share.