Inflation

Numbers over narratives

Current inflation is being compared to the 1970’s, which I don’t think is a good comparison. I will go over a few areas to see why. And I will focus on the US, since there is so much good data available.

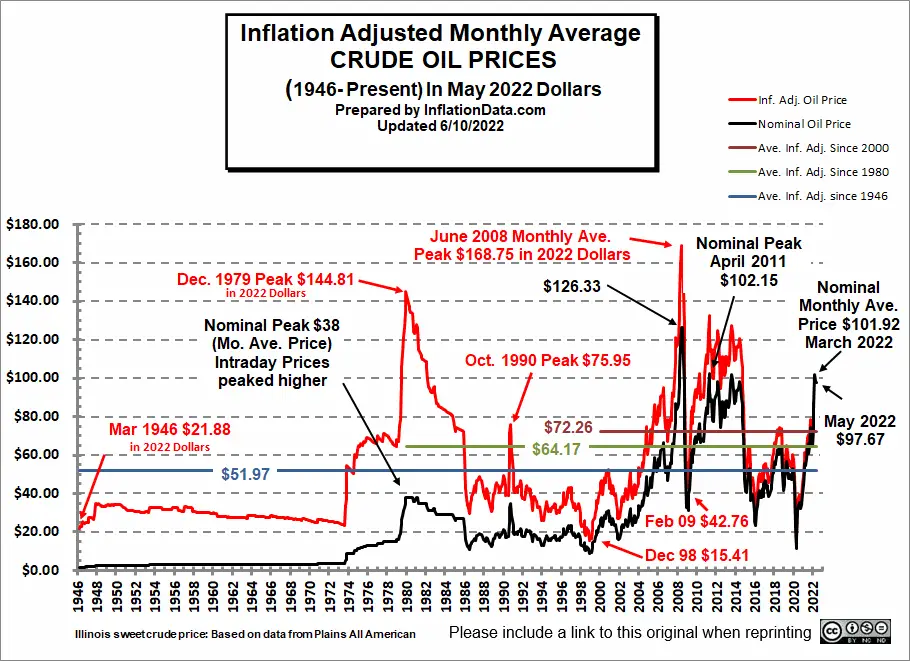

Let’s first get oil out of the way. The primary thing people focus on when discussing inflation. Since it was a major contributor to inflation in the 1970s. And demand is pretty inelastic. Nominal oil prices went up more than 10x from 1970 to 1980. Adjusted for inflation, they went up about 5x (source):

{kind=link}

Oil as a % of GDP went up from about 2% in the late 60’s to as high as 11-12% in 1980. Not hard to see how that can create double digit inflation.

Currently at $110/barrel, we are at 4% of GDP. With demand being less inelastic today as working from home, going electric and using Zoom is much more of an option than in the 1970’s. And we are still below the highs of 2010-2013.

So oil only plays a pretty modest role in the current high inflation. And the discussion around it seems more political than really based on facts.

What causes further inflation

You would think that if oil shoots from 2% of GDP to 10% of GDP, inflation would just be high for a year or two right? But that did not happen in the 70’s, it lasted for a decade.

That is because when oil goes up that much, industries have to increase prices, which causes a cascading effect which keeps going round in the economy. Workers will also demand higher wages, which in turn causes companies to again raise their prices, which then causes other companies to raise their prices, which causes workers to demand higher wages etc etc.

And as nominal incomes are increasing rapidly, the capacity to borrow also goes up almost as rapidly. Causing accelerating creation of new money. Historically most inflation was created by our fractional reserve banking system issuing new loans, thereby creating money out of thin air. And not by central banks printing money.

This process can keep going indefinitely. Which is why inflation can be pretty scary. Turkey had a 30 year period of double digit inflation.

Of course when it gets really out of control, then the central banks will have to print a lot of money to keep the government going. Which then causes people to try and get rid of their fiat currency as fast as they can. Which then causes more money printing and so on. Causing hyperinflation. But that is not really something to fear in the developed world. Since it only really happened once in Germany a 100 years ago, in pretty extreme circumstances.

How this time is different

I don’t think a repeat of the 1970’s is all that likely. There are several factors which will make this runaway inflation effect harder this time around.

They are:

Unionisation of the US workforce is ~10% vs almost 30% in 1970. So wages will go up slower.

Private debt/GDP is now at 160% vs ~90% in 1970. So less room for new debt creation.

Which also means interest rates do not need to go up nearly as much as in the 1970’s to cool down borrowing.

Corporate profit margins are almost double what they were in 1970, more room for compression there before price increases.

Shale oil has very high initial production, and short lead times. Which means higher prices create a stronger incentive for new production. And new wells are less risky, as most of the payoff is in the first few years. And new shale tech is yet to be fully utilised across the globe.

China stops overbuilding real estate, this currently gobbles up huge amounts of commodities.

And the bullwhip effect.

Demand shifted too fast during Corona. Too many people suddenly wanted to move to the suburbs. Too much sudden demand for semiconductors, lumber, camping equipment etc etc. Or it simply rebounded faster than expected like with autos.

All of that was infused with historically low mortgage rates and stimulus checks. Which caused clogged up supply chains, a shortage of container ships and a lot of industries suddenly gained a lot of temporary pricing power. Look how the PPI shot way up before oil went above a $100 (source):

This time around, it can be more quickly reversed into deflation, unlike the high oil prices of the 70’s and early 80’s, which took more than 10 years to unwind. As a lot more capacity comes online in 2023 and 2024. And demand shifts back to services again as we are leaving Covid behind us. A lot of industries might go into oversupply, bringing down prices.

Some of this can already be seen in trucking which saw a collapse in demand in the past few months.

So I would be careful to extrapolate from the past. We have only really been through 1-2 long term debt cycles with central banks in the past 100 years or so. And where you are in the cycle makes a huge difference. And how inflation is created also makes a big difference. The economic machine is now put together very differently than in 1970. In a way that makes sustained inflation less likely this time around.

Final thoughts

What I have not mentioned so far is deglobalization. I don’t think it is that big of a deal. Imports from China only account for 2.5% of US GDP. And there are plenty of alternatives to move factories to, like Central America or Vietnam. And this number won’t go to zero overnight (knock on wood). Of Course there is also automation which could cancel out inflationary effects of deglobalization over time.

I also don’t think the Ukraine war will have much of an effect. Russia will still sell its commodities as they need the income. They will simply sell it to some neutral country first, before they are mixed in with commodities from other countries and sold to the West. Nickel prices have already come down to February 2022 levels for example.

So my overall feeling is that these inflation fears are very overstated. And that things will normalize in 2023-24. The market is generally not a good predictor here. It panicked about crashing oil prices in 2016, about Trump, then changed its mind quickly. It panicked about Brexit, about the trade war, about Covid. In hindsight these were all great buying opportunities if you just looked at the numbers, instead of buying into narratives.

And most of my stocks have very strong outlooks for this year. Greif even increased their earnings guidance by 15% a few weeks ago. Extreme Networks has extremely strong order book etc etc. I suppose that is the biggest takeaway, don’t make any macro bets, just focus on the micro. And use this article to hopefully get a bit more peace of mind while doing so :) .

Further links:

Historical US inflation rates

{kind=link}

This was an amazing article, I loved how you shortened large topics into one sentence, and covered a lot of ground succinctly. I have to learn that trick ;)

I'm late to reading this but excellent article and I agree on all of it. Very bullish on stock moving forward