Tourmaline Oil

Perfect set-up for natural gas bull market

One of lowest cost producer in North America at $1.5/mcf FCF break even

Trading at >10% FW FCF yield at $2.8/mcf gas prices with >10% ROIC

Debt free by 2022

Depreciation overstated due to significant cost reductions in F&D costs in past years

2/3 of North American natural gas supply will show muted reaction to higher natural gas prices

Consolidation and investor focus on FCF will provide incentive against production growth

Let’s start with why Tourmaline is cheap. This is the current free cash flow outlook while growing production by 5% a year, natural gas price assumptions in fine print at bottom (source):

If you can’t read the fine print, 2023-2025 assume US$2.7-2.8/mcf natural gas prices. Tourmalines current market cap is about $11.5 billion.

These were the average NYMEX prices in the past decade or so:

Current natural gas price is about $4.6/mcf while rig count barely reacted and 2022 futures are closer to $4 compared to $3.2 assumption used above (source).

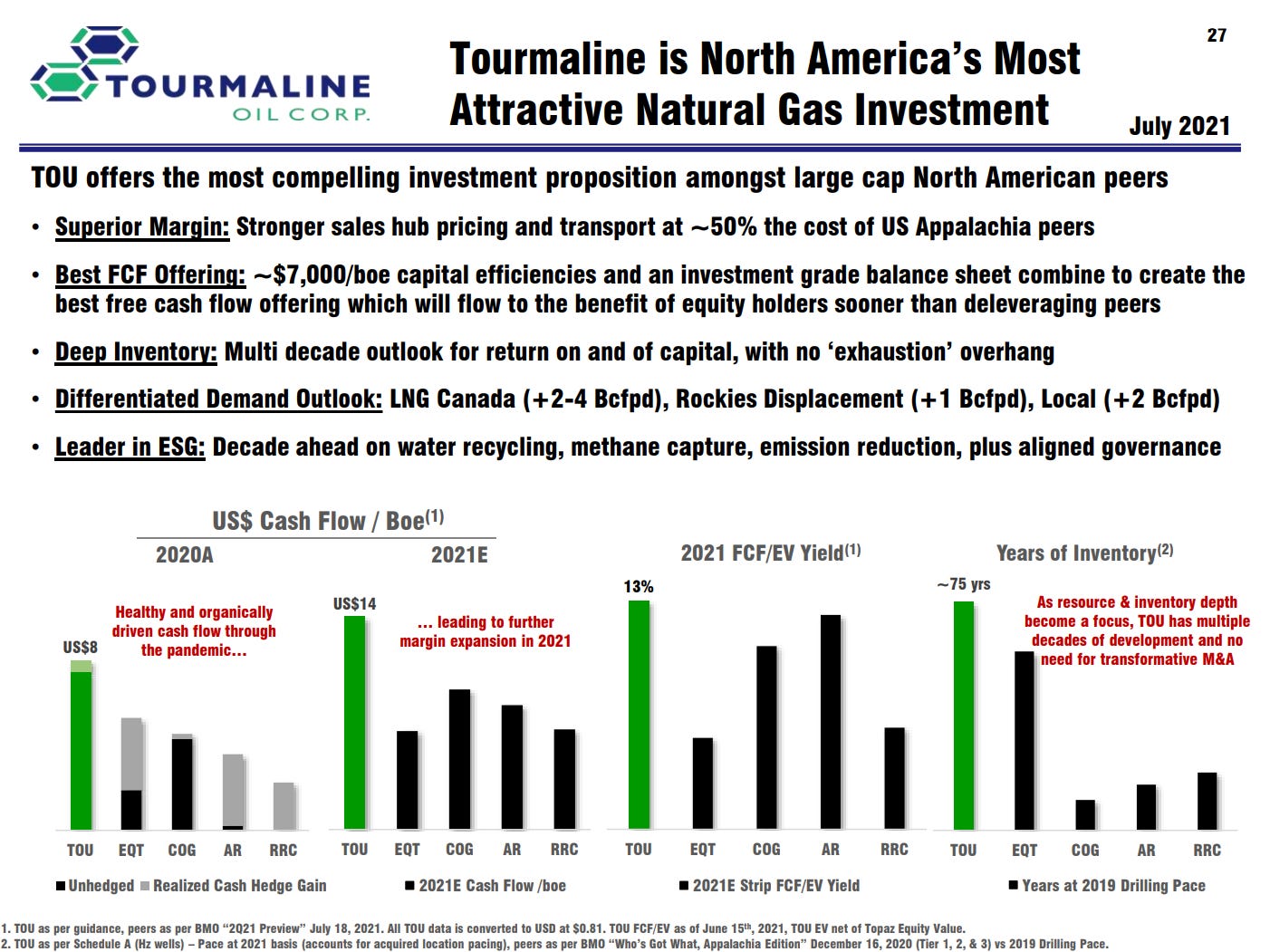

I don’t like to just paste powerpoint slides, but it does nicely sum up why this stock is attractive vs peers:

Tourmalines FCF break even price is estimated at US$1.5/mcf putting them on the low end of the cost curve. Depreciation also seems to be somewhat overstated as Tourmaline needs $1 billion in capex to keep production stable. The reason for this is that significant efficiency gains have been made in drilling wells in the past 5 years. Overall I get the impression that efficiency gains have been in the neighbourhood of about 100% for most natural gas producers due to faster drilling times and higher initial production and recovery.

Additionally Mike Rose, the CEO who owns 5% of Tourmaline, sold his last two O&G ventures for a very nice overall double digit return. Not hard to see how a cheaply priced producer with a 75 year reserve life that is a leader in ESG, would be an attractive acquisition candidate to one of the major oil and gas companies.

So with that out of the way, let’s see why the above estimates might be very conservative.

A natural gas bull market coming?

As a value investor I am extremely hesistant to try and call commodity markets as they are notoriously difficult to predict. But this situation just looks too juicy to ignore. In the near future about 2/3 of North American natural gas supply will be constrained either by muted oil prices or by a lack of pipelines. Creating a situation where high prices will not really result in much higher supply, unlike the past decade where producers went into “drill baby, drill” mode as soon as gas went above $3/mcf.

more than 1/3 of production in the North East of the US (Marcellus and Utica) is already close to being constrained by lack of pipelines due to a cancellation of a major pipeline last year (source):

Analysts at RS Energy Group and Gelber & Associates see potential constraints in Appalachia in 2022. Gas output in the region can grow by about 12% from current levels before maxing out pipeline capacity, said Matthew Lewis, a senior director at East Daley Capital Inc. He said a bottleneck could develop sooner if drillers ramp up production to make up for the loss of so-called associated gas, which comes as byproduct from oil wells in crude-rich basins like the Permian of West Texas and New Mexico.

“You run into capacity constraints at the end of 2021 at the current forward price for oil,” Lewis said.

There is only one significant pipeline coming online, the Mountain Valley Pipeline of about 2 Bcf/d. But even that is uncertain and already had heavy cost overruns and delays. Utica and Marcellus in the North East produce about 32-33 Bcf/d (source), or about 1/3 of all North American natural gas. Given how difficult it is to build new pipelines due to environmental activists successfully stoping them in court, it will be unlikely that significant future growth at least in the medium term will come from these two fields.

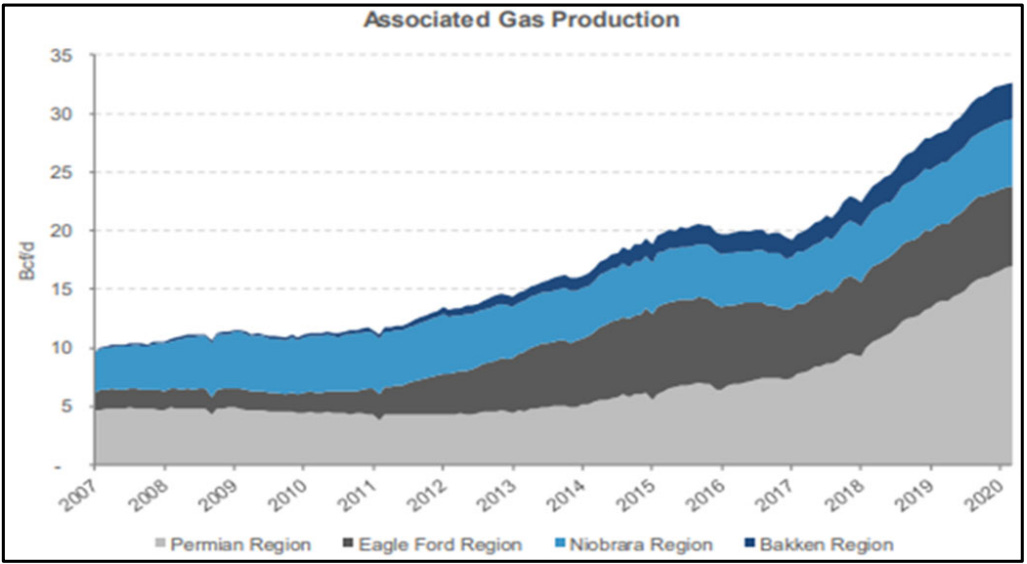

Then another 30 Bcf/d comes from associated gas (source):

Which will be constrained by muted oil demand in the medium term. 2024 oil futures already trade in the $50’s (source), and Permian producers need about $40-45 to break even. And OPEC conservatively has about 4-5m barrels/day in spare capacity vs about 96m barrels/day of consumption. Many oil and gas shale companies have mentioned high dividend payouts, low production growth and free cash flow generation in their presentations and conference calls. Unlike a few years ago when production growth was the major focus. Pioneer (producing ~15% of Permian output) management in Q2 call:

Scott Sheffield

Most of the numbers I look at, EIA has the highest numbers. They're at 11.85%. I think they're way too high. Most of the other tanks that I look at, they're around 11.5%. That's probably more realistic. But I'm still looking at about a 5% growth in the Permian, and most other basins will be flat to declining. And when you put all that together, we'll be lucky to grow 5% a year over the next several years in the U.S. lower 48. That's my general opinion.

And I think as more companies deliver their free cash flow model, they can't change it. So just like Diamondback committed to 50; the Cabot-Cimarex merger is committed to 50; Devon was committed to 50. So more and more companies, whether they commit to 50 or 75 , they're not going to change. And so I'm getting more comfortable with the fact they're just not going to grow that much U.S. shale, which helps.

Pioneer’s natural gas revenues in 2022 are estimated to only be 6% of their oil revenues. So higher natural gas prices will not incentivize them to increase production. And 5% estimated production growth is far lower than Pioneer’s 19% production CAGR between 2014 and 2020.

So really the only major field in the US that can provide significant growth in natural gas production and react to higher prices, is the Haynesville with current production of about 13 Bcf/day.

All of this while natural gas demand is expected to rise steadily by about 2-3% a year in the coming decade, to over 100 Bcf/day.

I think the skepticism of the equity market against natural gas equities, given that we come out of a nearly decade long natural gas bear market in equities, provides all this upside for free now. If I am wrong and Henry hub prices languish in the $2.5-3 range, Tourmaline will still generate >50% of its market cap in FCF over the next 5 years at a ROIC of >10% that can all go to investors. If I am right and current natural gas prices stay in the $3-5 range, Tourmaline might generate its entire market cap in the next 2-3 years.

I don’t know the probabilities here, but clearly the above scenario is hardly priced in:

Why Tourmaline specifically?

The entire natural gas equity market is actually quite cheap. Black Stone Minerals has major Haynesville royalty acreage and trades at a 2022 12% yield, and is debt free. I would be careful with North East producers like EQT or SWN. EQT has most of its production hedged anyway. And they still have significant debt.

In general my philosophy with commodities is, you either buy the best producer or royalties. Or maybe some high quality midstream companies (see my Rattler write up). And you want to do ok even if commodity prices dissapoint. So don’t pay more than 10x normalized earnings at conservative commodity price assumptions. And don’t buy levered commodity producers. If you mess around with levered producers that are higher on the cost curve, the thesis starts to really hinge on higher commodity prices.

In this case though, Tourmaline even trades at a cheaper 2022 EV/FCF multiple than for example Birchcliff or Peyto. Despite being of higher quality in every way. So you are not really paying a premium for quality. And nearly half of their revenue will be exposed to Henry Hub pricing over the next couple of years, despite being a Canadian producer.

So I am long Tourmaline at an average price of about $34 per share. And I may sell it at any time so DYOW.

More reading:

https://www.dallasfed.org/research/economics/2021/0304

https://marcellusdrilling.com/2021/08/m-u-will-run-out-of-extra-natgas-pipeline-capacity-in-next-2-yrs/

http://www.peyto.com/PMReport.aspx

https://www.spglobal.com/platts/en/market-insights/latest-news/natural-gas/033021-gas-production-growth-pipeline-constraints-leave-appalachian-cash-basis-lagging