Two new ideas

UK listed profitable OTC pharma stock with catalyst and Chinese retailer

I got two ideas today! A UK listed profitable and growing pharma stock (mostly over the counter) at 8x 2024 earnings with strong indications a PE buyout might happen soon (they have been increasing their stake aggressively this year and control over 40% of the company already).

And a large debt free Chinese ecommerce company, trading at 7-8x forward earnings returning >10% of its market in buybacks and dividends. With an artificially depressed stock price because of a large shareholder recently dumping its stake (you can probably guess this one fairly easily).

The first one is Alliance pharma (APH). They trade on the UK AIM exchange, but with pretty decent liquidity (for an AIM stock) and are buyable on Interactive Brokers.

They sell a variety of branded pharmaceuticals and don’t do meaningful R&D, all of their assets are gained through M&A over the years. The stock outsources manufacturing and a significant portion of revenue (35%) comes from one product, Kelo-Cote, a silicone scar treatment. Which is incidentally also the company’s expected growth engine over the coming years.

The market cap is about 200 million GBP with another ~80 million gbp in net debt by year end 2024. Overall past and expected future financial results from TIKR:

I broke down individual product categories over the past few years:

A breakdown of products:

Kelo-Cote seems like a leading silicone scar treatment that has double digit market share with significant room for future growth still. When the company acquired this product it had only 8 million in revenue.

Amberen is a meno-pauze symptom relief product. I am reading mixed reviews about it. APH had some setbacks on the ecommerce side with this product (7% share vs 20% in offline retail). There were various issues with this product like it not being sold for several months and suboptimal advertising. So it is expected that in the short term there will be some revenue growth followed by stabilisation as these issues have been resolved.

Nizoral is a product for severe Dandruff. China is about half of revenue and the company had some issues with marketing as well here and has changed its manufacturing partner this year. This has been resolved and some single digit growth is expected.

Then it seems the prescription side is made out of several products, some shrinking and some growing. Kind of hard to gauge. For example Macushield is a vitamin brand with flat revenue (about 9 million) and Hydromol eczema ointment also with 9 million of revenue and growing about 12%.

Overall I wouldn’t get that excited about this stock if it weren’t for the fact that DBAY, a British private equity fund has been aggressively increasing its stake directly and indirectly through Logistics Development group (LDG). DBAY went from 22% to 29% ownership earlier this year (at 30% I believe they will have to make an offer for the whole company). And LDG, which is managed by Dbay, increased its stake from 10% to over 13% in June this year.

So why do I think a buyout might be imminent? Well take a look at LDG’s holdings:

It seems LDG is used to get DBAY effectively over 30% ownership without triggering a mandatory takeover. And to increase odds of a buyout being approved. This happened with Finsbury Food, which is 13% owned by LDG and was taken out by DBAY for a 22% premium last year.

SQLI, which trades in France, had its public float reduced to <10% by a series of tender offers starting at €30 and ending at €44/share through Synsion (which is partially owned by LDG).

DBAY are shrewd operators, so I don’t expect a huge premium, but still a premium and it might happen before significant growth comes in next year. If adjusted earnings are 27-28 million the stock would only trade at a 7.5x PE. Say they are taken out for 11x earnings that means a 47% premium from the current share price of ~37p. Still far below the 70p it was trading at in early 2023.

What is the reason APH shares trade where they do? Well first they don’t screen very well as earning power has been obfuscated by 7 million GBP of acquisition intangible recurring amortisation charges and more importantly by the 85 million goodwill write-down of Amberen (only about 6% of revenue anyway).

Then there was the issue of a repeatedly delayed annual report this year and a management transition. Plus it is a micro cap pharma stock that trades on the AIM exchange in the UK.

I am long at 37p/share and will probably hold this for a year or so either hoping for a multiple rerating or a buyout from DBAY.

PS: LDG might also not be a bad hold here, they are buying back stock somewhat aggressively and DBAY has historically generated good returns. It is a way to buy cheap stocks at a significant discount. I expect their unlisted holdings to be relisted again in 5 years or so at a premium as that is the usual private equity playbook.

Then the second idea is… drumrolls… JD.com (JD)! I will not waste many words on this as you can find at least 5 write-ups (most recent one 2023) on VIC and countless more on Substack Twitter and other websites.

They are kind of the Amazon of China minus the dominant AWS business. The company is expected to grow revenue in low single digits, but EBITDA in the low double digits due to margin expansion:

“As we continue to invest with discipline in user experience and market share expansion, we expect JD Group's profit and profit margins to increase year-on-year. In the long run, we see a positive cycle between our business growth and profitability rather than contradiction. JD's business model is built on a robust supply chain and focus on user experience. We will make targeted investments in these areas to enhance user satisfaction and strengthen our market position, ultimately achieving long-term sustainable profits. We're confident in our ability to reach the goal of achieving high single-digit profit margin over the long term.”

I don’t know if that includes any special income, but EBITDA margins are currently at only 4.5%.

They are also aggressively returning capital, recently completing their $3 billion buyback and announcing another $5 billion one a few days ago. Together with a 3.2% dividend that is nearly a 10% yield this year and if they complete their $5 billion program (subtracting about $700 million of SBC), that would be a nearly 15% yield on their market cap in 2025.

The reason for the sharp drop (after the sharp rise after a great Q2) is that Walmart announced a sale of their entire JD stake, worth $3.7 billion.

So to sum it up, for $38 billion you get a dominant slow growing (mostly online) retailer with extensive logistics networks, $20 billion of net cash and investments (counting very conservatively) generating $160 billion of revenue and between $5-6 billion of FCF a year, buying back stock hand over fist, paying a 3.5% dividend (in 2025).

They say elephants can’t dance, but this is just too much of a bargain to pass up, especially with the large capital returns (that they actually seem to be doing and are not just talk).

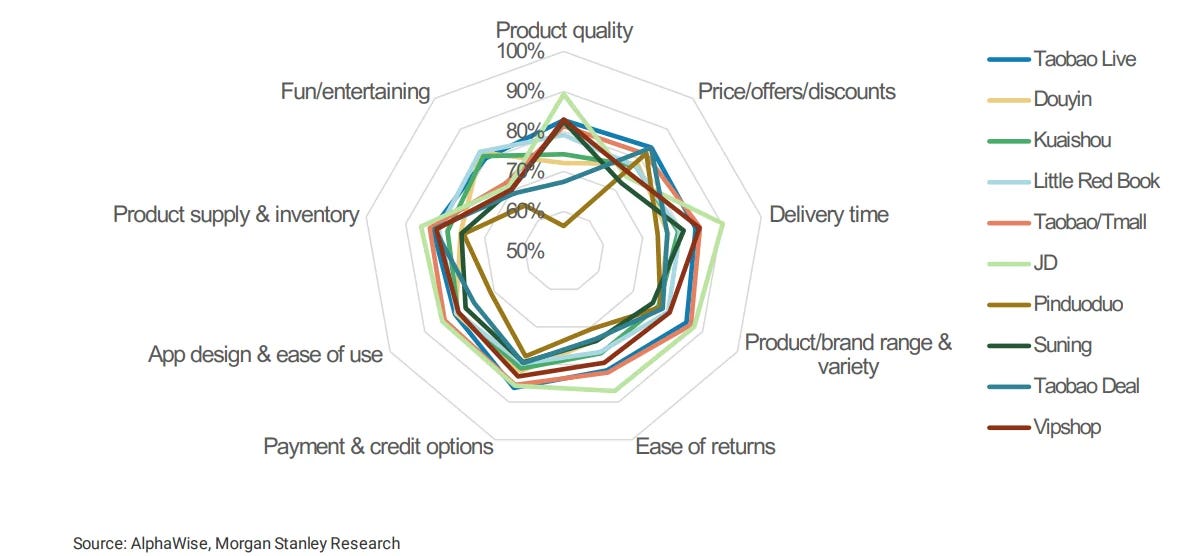

There is some concern about competition from Pinduoduo though, this graphic nicely sums up where JD differentiates:

I think Pinduoduo (PDD) might be more of a threat for very low value items, but higher priced items you want to have a middleman and cost savings % wise are going to be much lower. This is probably why JD is very dominant in electronics.

And I kind of struggle with PDD’s value proposition. So they let consumers buy in bulk directly from manufacturers while charging a fee for that. Vs JD buying in even larger bulk from manufacturers and selling it to consumers for a small mark-up? PDD also still takes a cut and it is nice to have a middle man that filters out the worst junk? If you care about quality, service and speed of delivery you may want to pay up a little bit for that?

For example I ordered a very cheap rubber brush a couple years back. It broke within 6 months. Then I bought a more expensive branded one and it is still going strong. Maybe when initial excitement wears off from people buying cheap crap on PDD, they return to higher quality retailers like JD?

Anyway here is some more interesting reading to make up your own mind:

What is behind PDD rapid growth?

Interesting reddit thread on JD vs BABA vs PDD

Thoughts on PDD after recent crash after very negative Q2 management commentary

Short write-up on PDD with a list of links to write-ups on JD and BABA as well

Disclaimer: Readers of this blog should do their own due diligence before buying or selling any of the mentioned stocks, since I have been wrong before and cannot guarantee all information in this write-up is 100% factual. I may buy or sell the above mentioned stocks at any time. Past success is no guarantee for future success. Some of the stocks mentioned might have poor liquidity, so make sure to check average daily trading volume before buying or selling anything. I am not your financial advisor.

Did you check Uni-Bio results? Very strong.