Greentree Hospitality

A forgotten Chinese reopening play

Greentree Hospitality (GHG) is a Chinese hotel franchiser and operator that trades at a large discount to other US traded peers and had some rumours floating around in 2022 that it would be taken private by its controlling shareholder who owns 88.7% economic interest in the shares. The controlling shareholder also indicated that the reason for its late Q1 2021 report was that they had hired capital market consultants to explore a take-private offer.

It does have some hair on it, but let’s first focus on the positives:

It trades at a large discount to US traded Chinese peers H world group (HTHT) and Atour Lifestyle Holdings (ATAT). Only at 6.5x 2019 earnings vs 60x for HTHT. (ATAT is a more problematic comparison). Also trades at a large discount to its historical valuation.

Actually hosts regular conference calls and seems more transparant than most Chinese companies.

The company has paid sizable dividends, more than 10% of its current market cap in 2021. $1.1/share vs $4 share price in 2019, 2020 and 2022 total.

Very high ROIC and wide margins due to a large portion of revenue coming from franchising.

Has net cash position (depending on value of franchisee loans though).

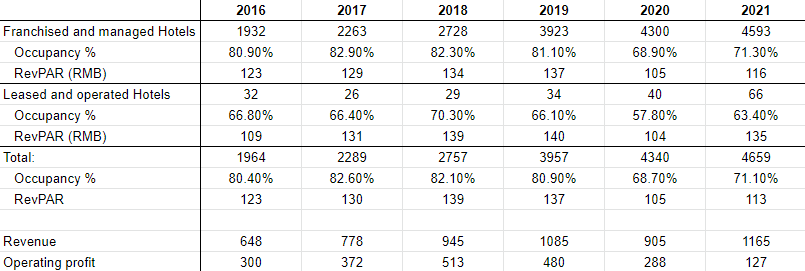

Additionally their operated and franchised hotel network has increased significantly since 2019:

What clouds the above figures a bit is that they have taken reduced franchising fees from their franchisees during Covid. But with their pipeline of new franchisees, total hotels opened could be over 40% higher by the end of 2023 vs 2019.

If earnings recover to 2019 levels (which seems likely now that Covid is over), and a 50% dividend payout is maintained then the dividend yield would be ~8-9%. With a possibility of a potential buyout if the shares do not recover. Or if tensions between China and the US heat up again.

Interestingly the shares traded between $10-15/share throughout Covid until the share price started collapsing in mid to late 2021. If it would trade at a historical discount with HTHT again, upside is more than 200% (orange is GHG and blue is HTHT):

The bad

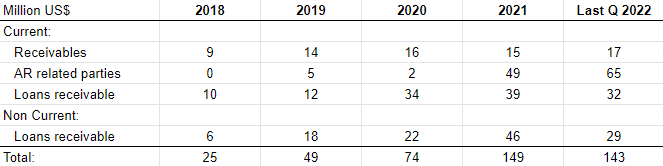

There is some hair on this stock that should be mentioned. Related party transactions and loans to affiliates have significantly increased in size during Covid:

They have also taken sizable losses on the loans to affiliates, $21m in 2021 and $51m in 2022 so far. I don’t think this money is stolen though, they seem to be propping up their affiliates, and either taking those losses intentionally (sharing the pain) or unintentionally (thinking they would recover these loans).

They also help their franchisees by taking reduced fees and no fees when they rent rooms to the government relating to Covid. This was about 17% of Franchisee revenue in 2021.

There are sizable loans out to catering companies controlled by the controlling shareholder of GHG. The big one being a bridge loan related to the acquisition of two restaurant companies from GHG’s controlling shareholder for the sum of $58 million.

It should be noted though that this acquisition comes with a guarantee of a compensation of $20 million if cumulative net profit of these companies between 2021 and 2027 is less than $20 million (so an average of at least $4m a year). And it is at least in the same industry? And supposedly there could be some synergies as well.

These are yellow flags and would be red flags if the controlling shareholder owned much less than ~90% of shares outstanding. And they would not hold conference calls and would not pay such large dividends. It doesn’t really make sense to steal from minority holders if you already own such a large portion of the company.

So I think the low relative valuation, dividends and the chance of a buyout of minority holders somewhere down the line makes this an interesting bet. Additionally the very low float could really make this stock fly if (hopefully when?) good news starts coming in. So I am long at about $4.1/share.

As usual, do your own due diligence before buying and I may sell at any time!

Thanks for the ideal, but I think relying on a private transaction that was rumored almost a year ago may not be realistic.