A review of 2024

First off, happy new year and a prosperous 2025 to everyone! Or is 1 week into the new year too late to do this?

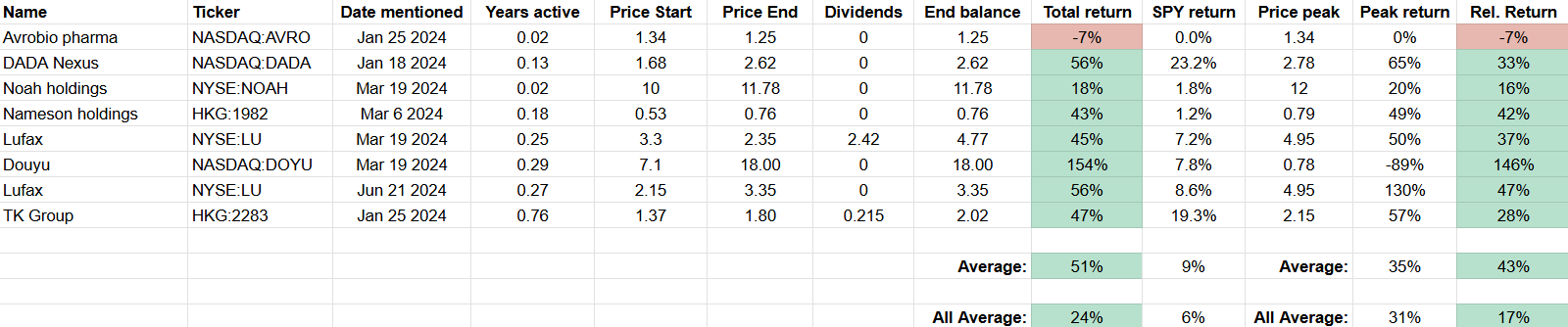

I have had a pretty good 2024, with 23 unique stock ideas posted (I don’t count Berry Global since I closed it right away). Average return of 24% over 2024, with 17% average outperformance vs SPY over the period ideas were active (probably subtract 1-2% since I did not count SPY dividends). 70% of ideas posted generated a positive return, and over half outperformed the S&P 500.

From now on I will increase the price of my paywall after good years, and decrease it after bad years (where I underperform). So starting on February 1 2025 the price for new annual sign ups and renewals will go up to €350 from €225 right now. I will lower it again if I underperform or have not provided enough ideas in a year. I don’t know if I can keep up this pace of new stock ideas. There are periods where I am in a dry spell, and then suddenly I hit a new vein and boom 3-4 new ideas in a month!

To get an idea of how much effort I put in paid write upss, I have removed paywalls from ATRenew and Protalix.

To see a more detailed table of my 2024 results scroll all the way down. For my overall track record since starting this blog click here.

I will post an update on all active ideas for paid subscribers.

Mistakes made

I made several mistakes this year, both by omission and by getting into a stock too early. At the start of the year when ATRenew (RERE) was trading at $1.1, I only bought a small position because it looked superficially cheap on several metrics. With a catalyst of renewed buybacks coming up. I should have loaded up at $1 instead, this cost me several %. I did not realize that this is actually a pretty moaty business with good long term growth prospects.

Then I got into DADA Nexus (DADA) too soon. I did profitably trade this with a small position but then entered back in at $2.35. I should have figured out that they were not done yet rolling out their free delivery program and they would cut ads to get more JD users more quickly.

Despite the bad performance so far, this is currently my highest conviction idea. Once advertising income comes back on their JD Now platform and user growth keeps growing well into double digits I think today's prices will seem like the bargain of the century a few years from now. It is hard to peg when it will happen and how much the company will earn exactly on top of this being a Chinese stock. So the market is now very much in wait and see mode and is trading like a net net.

I also wrote up VEON as a stock I did not own but probably should own 6 months ago. Had it on my watch list at $8 then I looked at it seriously when it was at $18, then posted my article in July thinking out loud that I should buy some shares at $26 (but didn’t) now the stock is at $45 lol. Basically the only reason for not buying was hoping it would get cheaper, which is a stupid reason not to buy it. At $18 the stock was trading at 3x growing earnings with debt EBITDA at only 1.6x with multiple positive catalysts in the near term. By far the cheapest EM telco/fintech stock out there. Even without the benefit of hindsight I was an idiot for not buying this.

I think I made the right decision closing Protalix (PLX), but then stopped paying attention to it. What tipped me over the edge towards selling was that their production facilities were very close to the border of Lebanon, and Hezbollah looked pretty scary in the middle of 2024 (now not so much). And I found out Sangamo basically has found a cure for Fabry disease. But it is not approved yet but it will likely be fast tracked.

Thinking it over now, I should have reopened it again in September/October when the Hezbollah threat went away. It will take many years for Sangamo to get their cure on the market and get it approved by insurance companies, and Protalix could easily earn $1/share for several years before that happens. The milestone payments for Elfabrio are $1 billion alone (vs <$100m market cap at the time).

Then in December Elfabrio started the likely approval process for once a month injections (instead of bimonthly) and is now being adopted as first preference with many health insurance companies around the world. This is a huge deal as it would cut the amount of annual trips to the hospital in half vs the competition (on top of the drug being more effective with far fewer side effects) than its only real competitor. So far the shares have more than doubled on that news, and I am gambling that I can get back in cheaper on a disappointing earnings release. Which has proven to be another mistake so far.

Galecto (GLTO) was a stock I should have sold sooner. I was hoping for a sale of their IP, but realistically it should have happened in H1 2024. So by May/June I should have sold my shares, or only kept a tiny position. My thesis after H1 contained too much hopium given the downside risk.

I wrote up Origin Enterprises (OIZ) in early 2024. But I stopped liking this idea. I think ROIC is simply too low for this business and growth is too low/choppy. From now on I want Return On Tangible Invested Capital (ROITC) to be at least 20%. The issue with such a low ROITC is that FCF generation will be too volatile, even though incremental ROITC is likely higher than 10% (on their landscaping businesses). I will keep it open, but sold in my portfolio on a small bump last year. By the looks of it, they will not generate much FCF this year, and capital returns will probably be limited.

SQLI was also a mistake of omission. I had a strong suspicion DBAY would come back and buy out the remaining few %, and it would happen somewhere in 2024. I looked at it in the middle of the year at 40 euros and thought “hmm I should buy some”. But then forgot about it and a month later it was bought out for 54. Reasons I did not get very enthusiastic were that finding detailed financials was rather impossible and the stock was fairly illiquid.

TUI AG (TUI1) was a mistake of laziness. I have had this on my watch list all year, but never seriously looked at it. My initial priors on it were that it is some trashy travel stock. They are mostly in hotels and cruises. The stock traded at only ~5x earnings in summer of 2024 making it a clear buy at the time given how tight hotel supply was/is in their geographies. The stock is still cheap, but not as cheap. A fair multiple is probably 9-12x earnings, currently the stock trades at 7-8x 2025 earnings.

Momentum trading

In 2024 I discovered that I am (or really should be) a bit of a momentum trader. At least while a stock is cheap and momentum is strong enough. Because I have this trouble that I usually have more ideas than room in my portfolio. So when to sell and when to buy something else that is cheaper? It would be rational to try to be in the cheapest stocks at all times right? To slowly sell down a position as it creeps up and not stubbornly hold on to 100% of your position until a share has reached your fair value target.

I think this is usually a good strategy. But sometimes when particularly good news has come out and when a stock prints one big green day after another I find that I turn into a momentum investor and hold on a bit longer even as a stock sometimes gets into expensive territory.

Until of course the stock starts trading sideways/downwards for a week then I start selling aggressively. Usually these aggressive rips come after good news (or after some rumor/inside info leak).

Here is a visual example of RERE’s graph, thick red and green lines are when I want to be 100% out/in of the stock, the black lines are the rips upwards. Rip 1 is announcement of a new buyback program, rip 2 news of a M&A guy from JD being elected to board of directors (plus good earnings), rip 3 was stimulus announcement, and rip 4 was another slightly better than expected earnings release:

I must admit though, I sold a bit too soon on rip 4. And sold too little after rip 3.

In between there are also upward/downward movements, but they happen more slowly often on no news where you should be slowly buying or selling the stock.

Plan and outlook for 2025 and beyond

I have made a mental switch in 2024 to put a bigger focus on earnings growth that is at least in high single digits and high ROITC of at least 20%+. Preferably with decent capital returns. And I don’t want to pay more than 10-12x FW earnings for it. So stocks like Origin Enterprises and Grupo Catalana Occidente no longer qualify.

With exceptions if a stock is particularly cheap (<4x earnings) AND is returning large amounts of capital.

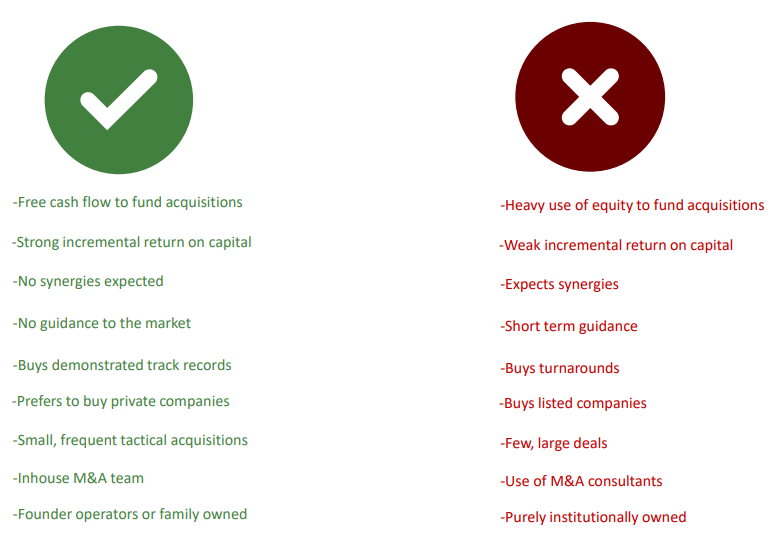

I have also added acquisition driven compounders to my circle of competence. This was an area I was a bit hesitant to invest in previously. What is nice about acquisition driven compounders (the good ones at least) is that they can generate consistent outsized growth for a long time in industries with GDP like growth. How to recognize the good ones? Well this checklist is a good start:

Source is this study by Req capital that I must have posted half a dozen times by now but it is a really good read, so I will post it again. I have identified a list of several dozen stocks that look interesting and have several currently in my portfolio (most of the recent write-ups).

My outlook is that European, Brazilian and Chinese stocks will probably outperform in the next few years. Stocks in those 3 countries trade at 7-9x earnings. The Brazil economy actually looks fairly healthy given all the pessimism, with 3% growth, 5% inflation, several $100 billion in forex reserves, unemployment at <5%. Despite interest rates at >10%.

Italy not so much, but within Italy there are growth markets that can be invested in at a cheap price like IT and fiber that are benefitting from sizable amounts of stimulus programs.

China will very likely announce large amounts of stimulus in spring 2025 to try and fire up the animal spirits again. Which is sorely needed if they want to prevent long term stagnation. Judging by their actions and policies, the guys at the top in China aren’t true communists. It was pretty funny this year seeing the market call for government stimulus while Xi Jinping was hesitant because he thought it would make Chinese people soft. While putting in place policies to incentivize stock buybacks. Supposed capitalists calling for socialism while supposed socialists are acting like American conservatives.

I am optimistic about European stocks overall. There is just way too much pessimism. It seems like Europe is kind of in the same place as the US was 10-15 years ago. The dollar was constantly weakening and everyone was wondering when the next terrible financial crisis would happen. I remember some economists at the time even floated the idea that the dollar could completely collapse overnight if it reached some kind of tipping point lol. Then the US came back with a vengeance.

Similarly I believe Europe will come back with a vengeance over the next decade. A move to the right is happening, and I hear a lot of talk on how to make Europe more competitive. Don't take my word for it though, European leaders are fully aware that we have a problem and seem intent on fixing it:

“The 27 member states at least agree on one thing: The need for administrative and regulatory simplification. German Chancellor Olaf Scholz called for a reduction in bureaucracy. "The Chinese innovate faster than we do, the US invests more than we do. And the Europeans regulate more than anyone else," a European diplomat said.”

Donald Trump might actually be a catalyst here, the threat of tariffs and no European wants to be outperformed by the US under Trump's leadership, that would just be too much of a loss of face.

You can say “well Europe is overregulated”. But you can also say “well discount to US is quite large, and there is a lot of low hanging fruit through deregulation to activate higher growth”. How much more easy and quick growth can be accessed in the US through deregulation? Probably much less. And you are paying a 100-200% premium with an expensive dollar.

That said, no value shitcos, quality companies only for me.

Results

Here is a list of my results, I only counted ideas posted this year, not still active ideas from previous years (the 4 worst performers are also my two highest conviction ideas for 2025, although Chinese pharma stock is no longer buyable on IBKR).

Currently active paywall ideas:

Closed paywall ideas:

Currently active free ideas posted this year:

Closed free ideas: