Berry Global, part II

Same valuation but now with improved fundamentals

Well apologies for not spacing out my blog posts better, but good ideas just seem to come to me lately. No paywall on this one.

This is a reactivation of an old idea Berry Global (BERY) that I wrote about 2 years ago. It is basically a roll up in the plastic packaging business.

The first rule of roll up investing is that you want organic growth. Without organic growth it will be hard to get long term returns or an earnings multiple above 10x.

I wrote this stock up in early 2022 and sold it 6 months later at $61 for a 13% profit just below where it is trading now. The reason was that organic growth wasn’t really materialising. In fact organic growth for BERY has been negative every quarter from late 2021 until Q2 2024. And there were some signs leverage wouldn’t come down.

Why I am more optimistic now:

Stock is still only trading at 8.5x 2025 adjusted earnings.

Organic volume growth (measured in tonnage sold) has finally turned positive to 2%.

Recycling rates are rapidly increasing, reversing potential terminal decline of plastic packaging.

New management planning to sell flat growth assets at or above current BERY trading multiple in 2025.

Exposure to higher growth consumer packaging and emerging markets has increased significantly.

BERY will really be close to a carbon copy now of Amcor but at nearly half the valuation.

So what has changed? Well organic growth (measured in tonnage of packaging sold) has finally turned positive to 2% last quarter and likely this quarter too and management is planning to divest underperforming segments and generate $1-2 billion in proceeds from that in the next 12-15 months. This will reduce net debt and further boost organic growth.

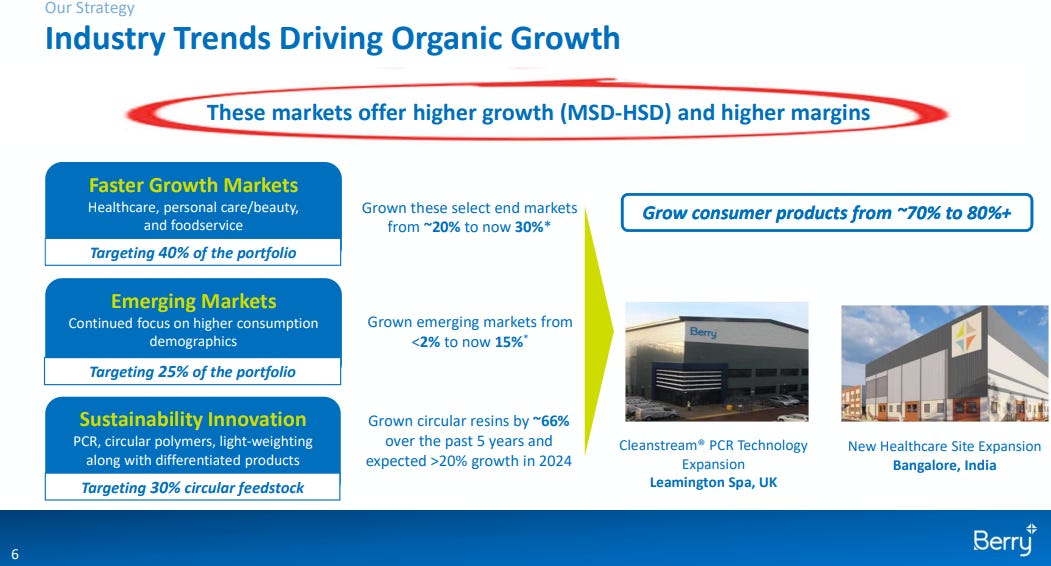

So 12-15 months from now we could be looking at more than 4 quarters of 2-3% organic growth, leverage in the low 3x possibly even high 2x EBITDA range and capital returns of another 5-10%. This slide nicely sums up the bull thesis:

This compares to Amcor’s currently leverage rate of 2.5-3x EBITDA and actually pretty similar organic growth in the past couple of years (BERY was hit harder by destocking and lightweighting):

Management is guiding for 2-3% organic growth, EBITDA growth of 4-6%, Adjusted eps growth of 7-12% and a total shareholder return of 10-15% in the medium term. Pretty similar to Amcor guidance.

If this is the case there is no reason why BERY wouldn’t rerate to Amcor’s multiple. A rerating to a 11-14x FCF multiple would provide 30-66% upside over the next 12-15 months, with pretty limited downside risk as organic volume decline seems to be mostly priced in already. And this business is fairly stable and recession resistant.

A recent VIC write-up (especially the comments) provide more details and are worth reading.

This VIC comment on why plastic packaging will likely not go into terminal decline I found quite insightful:

If the narrative around plastic packaging changes in the next few years, combined with some good numbers and cheap buybacks, it is not hard to imagine BERY outperforming the market.

Disclaimer: Readers of this blog should do their own due diligence before buying or selling any of the mentioned stocks, since I have been wrong before and cannot guarantee all information in this write-up is 100% factual. I may buy or sell the above mentioned stocks at any time. Past success is no guarantee for future success. Some of the stocks mentioned might have poor liquidity, so make sure to check average daily trading volume before buying or selling anything. I am not your financial advisor.

How do you feel about buying $AMCR now around $9.10?

Seems like a historically cheap multiple and they expect 3y EPS CAGR of 35% just from BERY synergies (so before any other growth into account)

The spin off still needs to happen, right? What do you think about buying before or after?